Toast Payroll: Get Help With Benefits Advance

Last updated: Apr 8, 2026, 10:04 AM

| This article should only be used by companies who do not manage benefits through SimplyInsured. If an employee who manages their benefits through SimplyInsured does not have enough funds to cover a deduction, the employer will not recoup the total premium for the benefit. The employer may decide to apply a manual deduction to the next payroll to recoup the shortfall. |

Benefits Advance

Many employees have the opportunity to enroll in employer-sponsored benefit plans. Often, employers will choose to cover a portion of these benefit premiums, which means the enrolled employees themselves share in part of the cost. The employer typically pays the full premiums directly to the carrier on a monthly basis. The employee portion is collected from regular earnings each payroll, effectively reimbursing the employer for a portion of the monthly bill to be paid.

Sometimes, employees do not have enough earnings on payroll to cover their employee premiums. In these cases, the employer has not received the full deduction from the employee, yet will still owe the full benefit premium at the end of the month. It can be difficult to identify and track these cases to collect the missed premium deductions from employees.

Toast Payroll will track these missed employee premiums. When an employee does not have enough paid earnings to cover certain deductions, the system will automatically add a Benefits Advance earning for the amount of the missed premium. This will happen during the payroll calculation process, giving payroll processors the ability to review Benefits Advance situations prior to submitting payroll.

Toast Payroll will use either a Benefits Advance or Benefits Advance (Taxable) earning code for this recording. The Benefits Advance (Taxable) earning code is used when the employee's pre-tax deductions exceed taxable earnings.

Note: The Benefits Advance and Benefits Advance (Taxable) earnings do not impact payroll cash requirements at all. They are simply a more transparent way to track missed employee premiums the employer likely wants to be reimbursed for from future earnings.

Note: In the case where an employee has zero earnings within a pay period, Toast Payroll will not be able to apply the original benefit premium (deduction) or a benefits advance deduction. This will result in a "missed" deduction and employers are responsible for tracking these situations if they happen to come up.

Example Scenario

An employee has a $50 medical deduction, but only worked 8 hours last pay period.

After taxes, the employee has $40 remaining to go towards the medical deduction. Instead of modifying the medical deduction to $40 (which makes it difficult to see that the employee did not pay $10 of their premium), Toast Payroll will add a Benefits Advance earning of $10 to offset the amount the employee was unable to be withheld. The medical deduction itself will record the full $50 employee premium.

If the employee earned less than $50 in taxable earnings, a portion or all of the Benefits Advance would be recorded on the Benefits Advance (Taxable) earning code.

This way, employers can easily:

- See when an employee has not had enough earnings to cover certain deductions.

- Collect missed premiums on a future payroll.

- Understand how much an individual employee owes in missed premiums.

Collect Missed Premiums

When an employee does not have enough to cover premiums on a particular payroll, the employer may wish to collect that missed premium.

After arranging with the employee, the employer can easily add a negative Benefits Advance earning to a future payroll to both collect the missed premium and to back out the Benefits Advance for future reporting. It is important to remember that the employee will need to have enough paid earnings to offset the negative Benefits Advance.

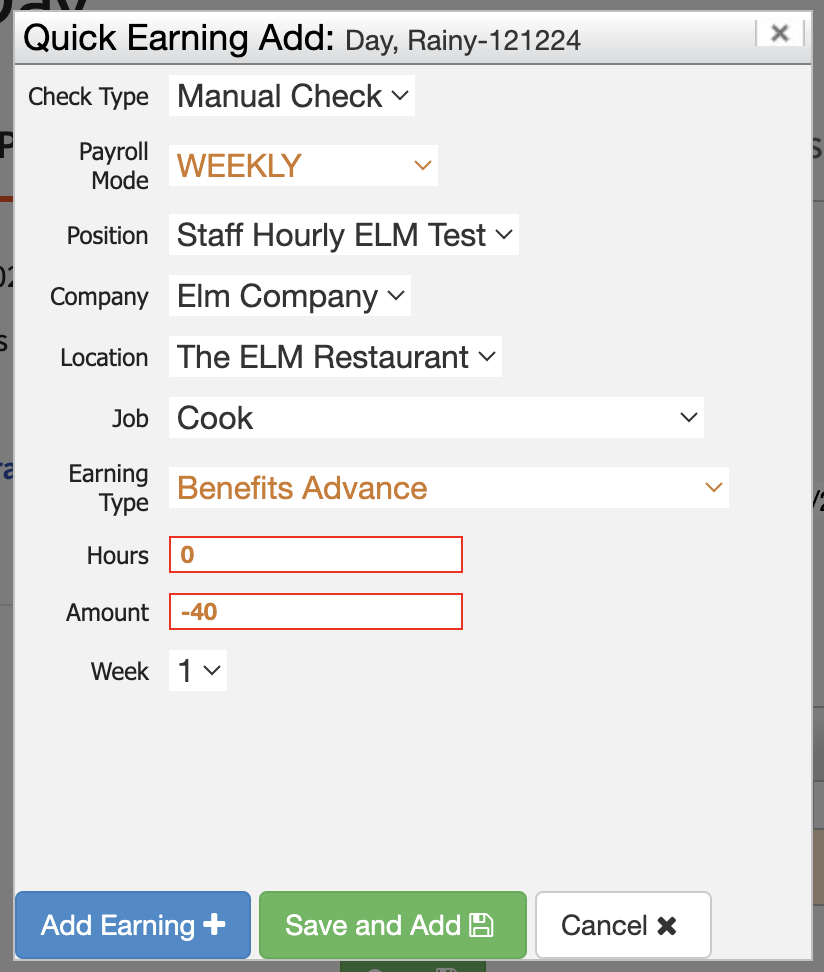

Adding a collection is done on the Employee Earnings step of payroll. Click here for instructions on adding one-time earnings and deductions to payroll. This is an example of what a $40 collection entry would look like:

If the employee typically does not have enough paid earnings to reimburse the employer due to high cash tips (see below), it is recommended the employer retain and pay some (or all) of future tips on a future payroll in order to be able to withhold from those tips the outstanding Benefits Advance.

How Cash Tips Impact Benefits Advance

In addition to times when an employee simply did not work very much in a particular pay period, cash tips are one of the most common reasons this situation arises.

For employees who receive the majority of their pay in the form of cash tips throughout the pay period, it is very common that they don’t have enough earnings paid on payroll to cover deductions. This is because these cash tips are fully taxable, and the resulting tax liability often consumes any earnings actually paid on payroll. This leaves the employer unreimbursed for certain deductions.

The Benefits Advance earning will help employers track these instances. But ultimately, transitioning to paying some (or all) cash tips on payroll will significantly reduce the cases when employees cannot satisfy all deductions.

This content is for informational purposes and is not intended as legal, tax, HR, or any other professional advice. Please contact an attorney or other professional for advice.